Last week a real estate investment trust (REIT) – which was not financially stressed – voluntarily “turned in the keys” for one of its properties, defaulting on a $725 million loan. The ramifications of this decision depend on a lot of factors.

Let’s talk about what it means for you.

On June 5, Park Hotels and Resorts (PK) announced it would stop payments on a $725 million, non-recourse CMBS loan secured by two of its San Francisco hotels. The hotels are the 1,921-room Hilton San Francisco Union Square and the 1,024-room Parc 55 San Francisco.

The press release made these comments:

After much thought and consideration, we believe it is in the best interest for Park’s stockholders to materially reduce our current exposure to the San Francisco market. Now more than ever, we believe San Francisco’s path to recovery remains clouded and elongated by major challenges—both old and new: record high office vacancy; concerns over street conditions; lower return to office than peer cities; and a weaker than expected citywide convention calendar through 2027 that will negatively impact business and leisure demand and will likely significantly reduce compression in the city for the foreseeable future. Unfortunately, the continued burden on our operating results and balance sheet is too significant to warrant continuing to subsidize and own these assets.

There is a lot here to unpack.

A non-recourse loan means that Park Hotels can literally “turn in the keys” and not have any further loan obligations. The company said it would work with the loan servicers to determine the most effective solution.

The loan was part of a commercial mortgage-backed securities (CMBS) pool. This structure means any investors in the CMBS will be negatively affected.

For the REIT, stopping payments on the debt will reduce the debt-to-EBITDA ratio from 6.0 to 5.1. The company expects to save $30 million of annual interest expenses and $200 million of maintenance CapEx over the next five years.

The cash savings will let the company pay a special dividend once the hotels are fully out of the portfolio.

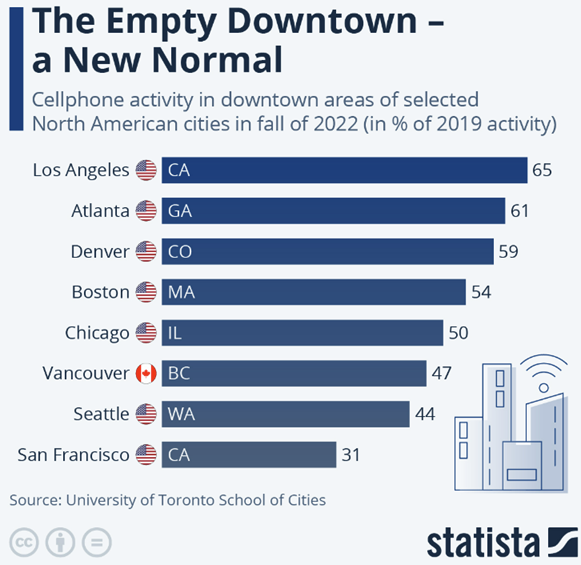

For the larger picture, investors need to know where REIT properties are located. There is a mass business exodus out of San Francisco, so REITs with heavy exposure to that city or others with challenged business environments should be sold or avoided. This chart uses cellphone activity to show which downtowns have recovered the least from work-from-home policies.

Commercial mortgage investors are at significant risk. Banks, CMBS, and finance REITs own these loans. CMBS are typically by large institutional investors such as insurance companies and pension plans. Stay away from riskier finance REITs. There will be companies that can take advantage of financially stressed situations. Starwood Property Trust (STWD) has a long history of finding special opportunities in commercial finance.

Finally, this decision makes Park Hotels & Resorts a more attractive investment. I will keep a close eye on this lodging REIT.