Ask any old trader whose enjoyed any level of success, what’s the secret to their longevity and it will most likely be some variation of the ‘R’ word… Risk.

You can employ any combination of strategies and methodologies, but without them being joined at the hip, neigh ruled, by a strict set of risk management tools, failure is already a forgone conclusion.

One of the easiest ways to do that is to use the “R” method, which was developed by Brian Lund.

For Lund, “r” represents a fixed dollar amount, which represents both the risk and reward you’re willing to accept on each trade. This will properly allocate individual position size within your overall trading account, as well as how much of that trade your risking, or willing to lose.

It is best arrived at by using a percentage of your total trading capital. It allows you to size your position in relation to your risk level instead of in an arbitrary way.

For example, if you have $50,000 available in trading capital (cash not including margin), you might use one-quarter of one percent (.0025), or $125, as your “R” factor. Take that one step further, the total amount you are willing to risk per trade, such as 20% loss on that trade where you are using that $125. This means you are ultimately risking $25, just as an example of how risk management should work.

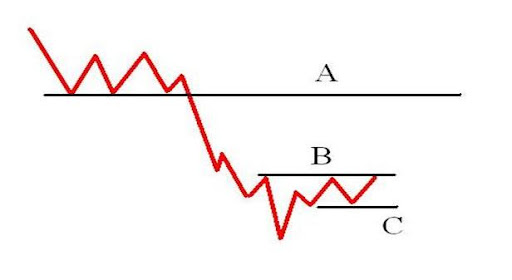

In the highly technical example below, (A) is a former support level that failed and now is a potential resistance level.

Price is trapped between (B) and (C) level, and you are looking to go long if it breaks back above (B).

You know that a reasonable stop-loss would be just below level (C), so you determine the price distance between your entry just above (B) and your stop just below (C).

Let’s say that this distance is 50 cents. You now take that distance and divide it by your “R” factor, which gives you a position size of 250 shares ($125 / .50 = 250).

You now know that if your trade fails and hits your stop-loss, the most you can lose is $125. The goal then becomes to only take trades where you have the best potential reward for the risk you’re putting up, ideally 1:3 (risk to reward).

In this same example, the resistance level of (A) is a reasonable target for a successful trade, so you determine the distance between your entry just above (B), to the target of (A). You then divide this number by your “R” factor to see if the trade is worth taking.

If the distance between (A) and (B) is $1.50 then you have a 1:3 risk/reward ratio and the trade is a good bet ($1.50 / .50 = 3).

The higher the risk/reward ratio you have on your trades, the fewer times you have to be right and still make money. One South African firm only won 30% of their trades, but was still wildly profitable, due to proper risk management.

As you can see, if you only take trades that have a 1:3 risk/reward ratio, you only need to be correct 50% of the time to have a 10R profit after ten trades.

Knowing how to use risk/return and position sizing allows you to make sure you are never overextended on a trade and ensures that you’ll always be able to return to fight another day.

Risk management is just one of the various trading topics I go over routinely with my students in the Options 360 trading community.

If you’ve been looking for world-class trading education, check out this short presentation to learn more about my trading methods and how joining the Options 360 community can help take you trading to the next level!